Summary

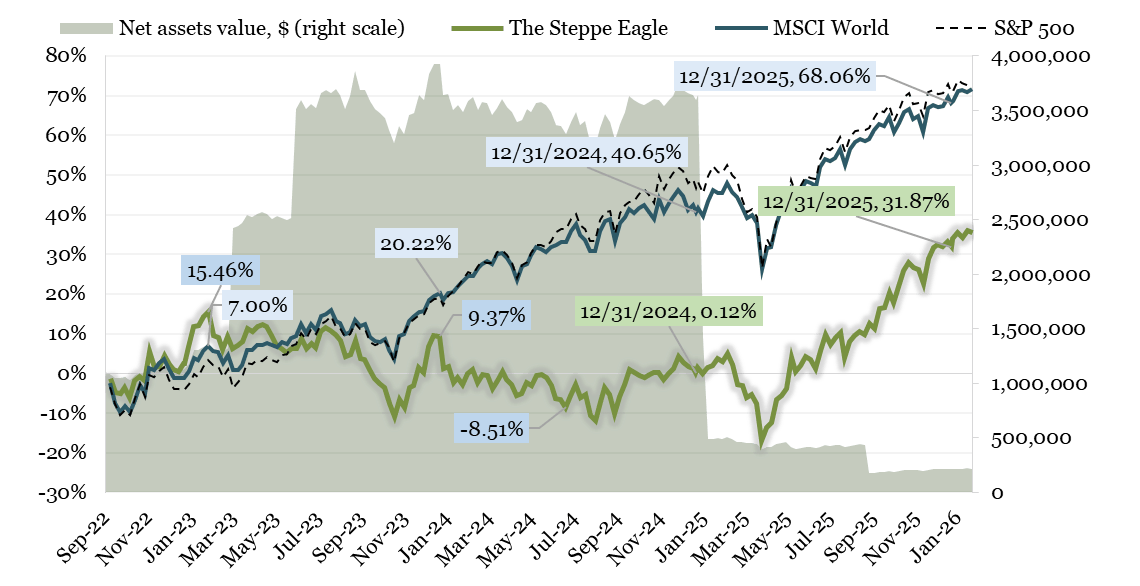

- The Steppe Eagle OEIC Ltd delivered a strong +31.71% return in 2025, outperforming the MSCI World Index by 12.22% for the year.

- GOOGL, initially seen as lagging in AI, rebounded with Gemini and Anthropic, though current market enthusiasm may be overextended.

- SaaS sector faced an unexpected ‘apocalypse’ in late 2025, with Salesforce and peers suffering sharp valuation declines amid AI disruption fears.

- Solar and wind holdings rebounded sharply in 2025 after a brutal downturn, validating patient, value-driven accumulation during sector distress.

Nico De Pasquale Photography/DigitalVision via Getty Images

Fellow Investor, Unitholder, Reader,

The author is delighted to be with you after another round, another year. In Harry Qelm Baabsman we treasure your curiosity and preparing hard for your attention; if you like what you’re reading, please say so, that would mean a lot. We talk about investment results openly, explaining unpleasant and fortunate choices that sometimes switch places by the grace of Mr. Market’s flimsy behavior. The last couple of years have been rather ironic. Patience is the first condition for our fund, we aim at the investment horizon of 3, 5, and 10+ years because investing is a long story.

The stock market, at times, tests the managers’ very trust in themselves and makes them question their competence. Yet patience and work eventually get rewarded. 2025 was the first prominent year for the Steppe Eagle with a flash performance of +31.71%. The 2024-loser sector of clean energy has turned the tables and come back tough in the second half of 2025.

Dynamics (Harry Qelm Baabsman Ltd.)

The Steppe Eagle OEIC Ltd was registered on 25th of July 2022; Started its operations on 8th of September 2022 and is managed by Harry Qelm Baabsman ltd, a CIS License holder at AIFC (AFSA-A-LA-2022-0006, active since 3d of February 2022). On 31st of December 2025, The Steppe Eagle consisted of 16 158 120 Units; the Unit’s price was $0.01319.

The Steppe Eagle finished 2025 with a gain of +31.71%, whereas the benchmark, MSCI World Index, yielded +19.49%. Since its inception, the Steppe Eagle has arrived at +31.87% versus +68.06% for its benchmark. Since September 2022, inflation in the US (CPI) has accumulated to 10.02%.Thus, the Steppe Eagle soared above its benchmark by 12.22% in 2025 but is still 36.19% below it since the Fund’s inception.

We all are swimming in a sea of surprises, which empties numerous rivers of probability; some probabilities seem certain until they don’t, some catch us fully off guard. All we do is keep our raft along sure streams, trying to act reasonably. When shocks unavoidably get us, we check our math and our heads, we get several clues of what we could have done differently, but most of the time we are dealing with events that are impossible to foresee, let alone make investable conclusions. We just learn to be extra cautious. Let me present just a few examples.

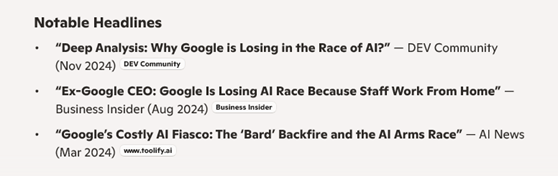

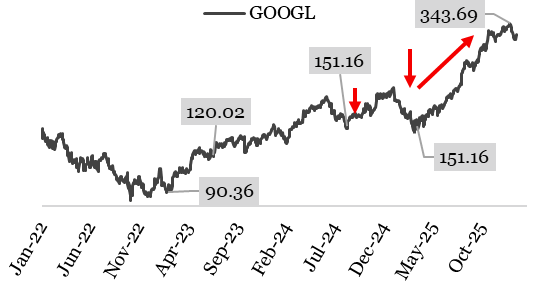

First. Alphabet (GOOGL) was perceived by many as a loser in the AI race just a few years ago, with its failing Bard AI, far behind OpenAI backed by Microsoft (MSFT), Tesla’s Grock (TSLA), Anthropic, and several LLMs from China. But recently, with the advance of the new generation of Gemini and its investment in Anthropic, Alphabet was crowned as the ultimate winner of the race. Could be true, could be false, time tells. I am just highlighting that this turn of luck was close to impossible to foresee.

Headlines (Harry Qelm Baabsman) Alphabet (Tikr.com)

After the broad market crash in late 2022 and succeeding recovery, GOOGL stock went back and forth between $150+ and $180+. The market ignored the company’s lean, stable growth; it focused on the AI story. We didn’t expect any AI bonuses; we have held the stock since late 2022 because it was a solid, thriving business. Not sure it deserves the laurels the stock enjoys now; all we wanted was a 10-15% annual return.

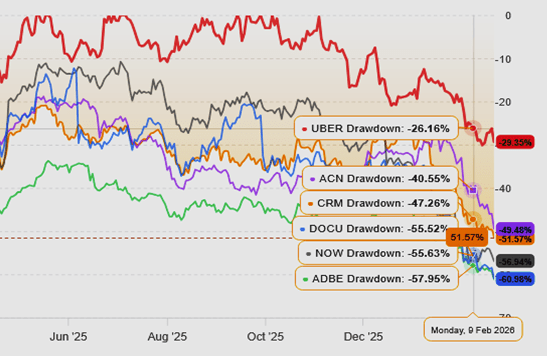

Second. In February 2026, someone coined the term “SaaS-apocalypse” to describe the market shift that began deep in 2025. Once beloved and desired “Software as a Service” companies, highly profitable and highly scalable, are now being threatened by advancing Large Language Models (LLMs or AI, as news call them). Adobe (ADBE), Salesforce (CRM), Docusign (DOCU), ServiceNow (NOW), etc. All have been losing their market capitalization like it was the 2001-2003 or the 2008 crisis. The wave is flashing down Shopify (SHOP), Accenture (ACN), and Uber (UBER) along the way (why Uber?). Who could have predicted it just a year or two ago, when those companies stormed their all-time highs? Maybe someone did, but we are not there yet to forecast multi-decade trends to falter.

SaaS-apocalypse (Tikr.com)

These companies were praised by the public & experts. They still enter the lists of companies with the highest marginality due to the nature of the SaaS business model. Nevertheless, back in May 2025, we had no idea what massacre would happen within 6-9 months. Fast-forward to the present: that inflicts a bit of discomfort for The Steppe Eagle, especially Salesforce, our long-term favorite, lost 45% from its highs of $320+.

That was another surprise that we have to deal with, we didn’t know this wave would come. One tool to thread lightly is: we can buy 0.5-1% of each profitable, healthy company every 20-25% drop and wait several years, as with Alphabet or Shopify (SHOP). As most fears go, but not all though, these could also be overblown; time will tell.

Third. Starting this letter with “…unpleasant and fortunate choices that sometimes switch places by the grace of Mr. Market’s flimsy behavior” we meant Solar and Wind energy.

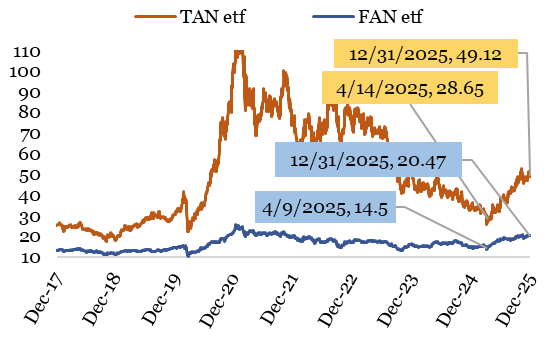

As you, dear readers, know, The Steppe Eagle was designed to benefit from this emerging multi-decade tendency that rapidly and surely shifts the way humanity obtains power for almost all needs. Not only that, but to promote a more harmonious way for business and the planet. It is cleaner, cheaper, and better for our future. Once in a decade or so, this sector gets its beating, a bad one. Before the bloodbath we experienced in 2023-2024, the previous was in 2012-2014, the post-Fukushima nightmare; mid-quality went bankrupt, best companies lost 75-90% of value, bad ones perished, and history doesn’t remember their names. Back in 2022-2023, when making investments, we weren’t expecting that a strong sector, in terms of Gigawatts and billions of USD, would simply stop for good for long 18 months and start losing revenues. It did. The sum of revenues of the companies included in Invesco Solar ETF (TAN) grew from over $30 billion in 2020 to over $64 billion in 2023, or 28% a year, as the compounded annual growth rate suggests. And cumulative assets changed from $120+ billion to $180+ billion; not bad at all. What more important is, that kind of dynamic can be traced back to the pre-2008 financial crisis. When prices for SolarEdge (SEDG), Enphase (ENPH), Vestas Wind Energy (VWDRY), Canadian Solar (CSIQ), Shoals (SHLS), Nextpower (NXT), etc. reached sound valuations in 2023 and especially in the third quarter of 2024, the Fund bravely invested in this familiar, fund-specific sector. We had no idea what kind of surprise we would eventually get. That cost us dearly, in terms of business and self-esteem. However, in the second half of 2025, the Solar and Wind reported for duty (well, it was about time!). The first surprise was totally unexpected; even long-term investors don’t live and make decisions based on fears of what happened 10-15 years ago (we are only humans). The second surprise, the recovery, was hoped for, but wasn’t certain. We’re happy we bought in; some of the stocks doubled or tripled in 2025, like Nextpower, Shoals, and Fluence Energy (FLNC). God willing, this sector is still our future.

TAN & FAN ETFs (Tikr.com)

A few figures: a) TAN etf lost -26.82% in 2023, -37.92% in 2024, and gained +48.31% in 2025; b) FAN etf lost -4.85% in 2023, -10.19% in 2024, and gained +38.31% in 2025.

As the chart below shows, the solar sector is uneven and does not progress coherently, however some companies are thriving, and our job is to spot them and keep them, sometimes getting thorns along with roses, but roses as well.

3y CAGR

5y CAGR

7y CAGR

10y CAGR

15y CAGR

TAN etf

-12.35%

-13.72%

14.93%

4.83%

-2.61%

FAN etf

5.73%

-2.56%

8.64%

6.07%

4.72%

Click to enlarge

Concluding this part. Mr. Market cannot be trusted, do not believe either his words or short-term actions, but do believe in your expertise, hard work, and be patient. Mr. Benjamin Grahham the Dean of Wall Street, said it best:

You’re neither right nor wrong because other people agree with you. You’re right because your facts are right and your reasoning is right—and that’s the only thing that makes you right. And if your facts and reasoning are right, you don’t have to worry about anybody else.

A wider perspective

As usual, describing the year, many say, “What a ride!” We have had the chance to witness how the “Trump card” has wildly changed players’ fortunes. There is a good saying whose original author is unknown, so there are many variations of it. Here is one of them: Expect the unexpected and prepare for the inevitable.

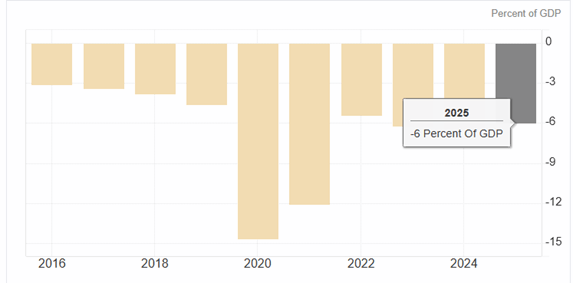

Mr. Trump and Mr. Musk started something together, then split their ways with doubtful success in budget deficit cutting. The POTUS’s Office introduced the “Reciprocal Tariffs,” which hit the markets in April 2025, but then the Office demonstrated tactical flexibility with those tariffs, and the current state of this question is a puzzle and a mess. Just one chart on the budget deficit. Nothing changed.

budget deficit (tradingeconomics.com )

The current US Administration has been the main news maker since November 2024. Yet data and figures live their own lives. The inflation rate is not at the desired 2% level; it is just below 3%, supported by higher import prices (the US is the largest importer of goods and services in the world, over $4 trillion), so the high interest rates by the FED are justified.

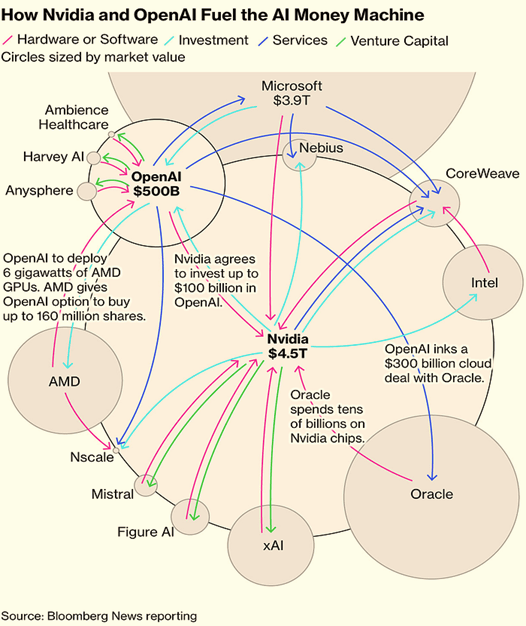

The “Magnificent 7” craze finally lost its appeal in 2025; the companies took their own paths. Only Alphabet, Meta (META), and Nvidia (NVDA) remained firm. However, something shady is happening between all those AI and microchip companies; it is called “Circular spending”, when sales are not created by customers’ spending but rather by cash changing hands among the same group of entities. Stagnant or deteriorating cash balances of those companies confirm some truth in that theory. Nvidia’s cash & near-cash items increased just 2 times in 3 years, yet its operating income jumped 4+ times; it sure reinvests a lot, but the company doesn’t get as much real cash as its sales’ dynamics suggest. Alphabet’s cash & near cash didn’t change over 3 years, despite huge operating income growth over the same period. Sure, it spends a lot on CapEx and R&D, but there should be a bigger cash impact from all that income. And Microsoft’s (MSFT) cash & near cash fell during the last 3 years, despite 60% sales growth. Something doesn’t add up. However, a full study of this matter would take an unbelievable amount of time. We remain a notch skeptical, especially in light of the following chart.

That interdependency always puts most participants in a vulnerable position, if something goes wrong; sooner or later, it does. We can’t say what proportion of those companies’ sales actually consists of good old cash.

Chips & AI cycle (Bloomberg news reporting)

This chart is part of an article at Medium, “The AI Bubble: How Circular Spending Is Inflating America’s Newest Speculative Frenzy”. It must not be the complete truth to serve as a reason for a good deal of cautiousness. It tells exactly this:

Back in the late ’90s, we had the same thing. Vendors would finance their customers’ equipment purchases, then count that as revenue. The customers would use the money to buy more equipment, inflating the vendor’s sales figures. It worked brilliantly until everyone realized there were no actual end users paying real money. Then it all collapsed like a house of cards in a windstorm.

This chart is part of an article at Medium, “The AI Bubble: How Circular Spending Is Inflating America’s Newest Speculative Frenzy”. It must not be the complete truth to serve as a reason for a good deal of cautiousness. It tells exactly this: “Back in the late ’90s, we had the same thing. Vendors would finance their customers’ equipment purchases, then count that as revenue. The customers would use the money to buy more equipment, inflating the vendor’s sales figures. It worked brilliantly until everyone realized there were no actual end users paying real money. Then it all collapsed like a house of cards in a windstorm”.

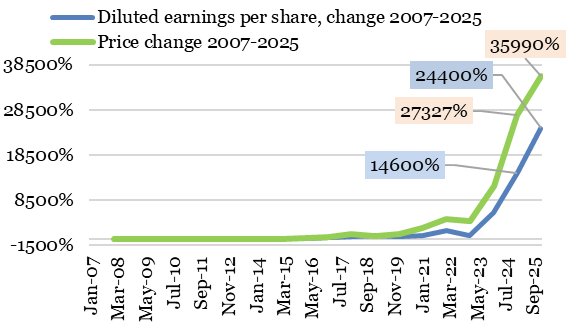

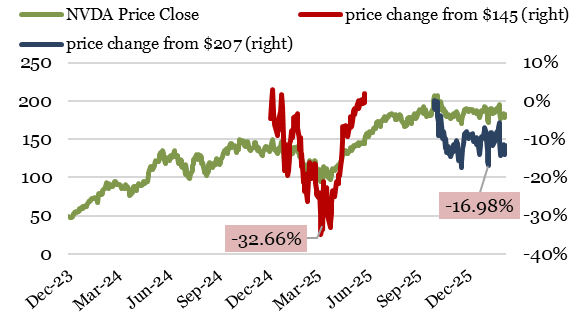

Someday we stop revisiting Nvidia’s Income statement, but not today because we have front-row seats at this show of unsafe valuation. Once again, there is a stretch between the growth of earnings per share and the stock price. As we always repeat: …from a historical perspective, these two metrics should align. In order to justify such a change, the company should more than double its earnings without any price change, or the price should decrease by at least 50%.”

In the spring of 2025, NVDA fell to $95 per share, down from $145 in late 2024, approximately -50%. Today, the price is $185+, but the company’s revenue growth has cooled from over +114% in 2024 to +65% in 2025. It is very reasonable to expect a weaker performance in 2026-2027 from this investment, even if the “Circular spending”-doubts were 100% false.

Nvidia’s EPS & Price (Tikr.com) NVDA price drawdowns (Tikr.com)

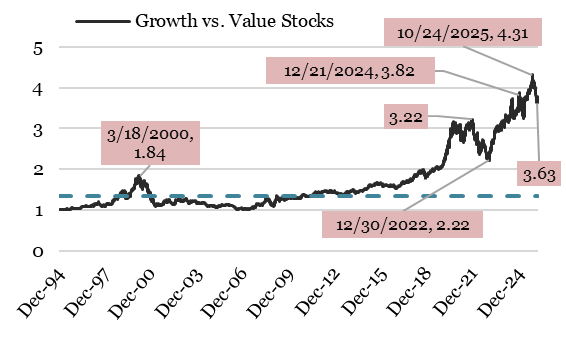

We monitor the Growth-to-Value stocks ratio since early 2024 (see the Investment report for FY 2024). Though exciting and promising new technologies may be, they still need the backing of tangible hardware and electricity. And as 2025 made clear, the data centers that train & use neural networks consume a gargantuan amount of energy, but the power grids in many developed countries proved insufficient. More capacity and, thus, investments into infrastructure down the chain are required. The curve below still doesn’t look promising for the growth stocks in the next 5-7 or even 10 years.

Growth vs Value etfs (Tikr.com)

Our moderate positions in the old-fashioned value stocks have been successful so far. We started picking them at the end of 2024 & early 2025; they looked cheap compared to their historical multiples. Still not sure the turning point has actually occurred, but let’s see what happens over the next 3 years.

12/31/2023

12/31/2024

12/31/2025

2/27/2026

BorgWarner Inc (BWA)

35.85

31.79

-11.32%

45.06

41.74%

57.57

27.76%

Magna International (MGA)

59.08

41.79

-29.27%

53.3

27.54%

63.05

18.29%

Thor Industries (THO)

118.25

95.71

-19.06%

102.67

7.27%

96.13

-6.37%

Click to enlarge

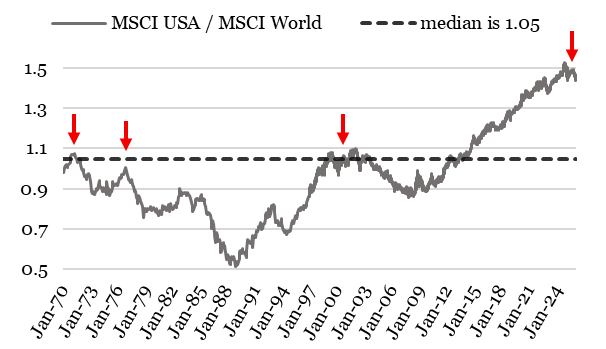

Let’s revise the next good old “USA stocks vs World” chart. The relative strength of American companies is staggering; however, each step up takes more effort, and now the gap between their valuations is entirely unreliable. No wonder the MSCI World Index outperformed the S&P 500 in 2025: +19.49% versus +16.38%. At some point, it breaks.

MSCI World vs MSCI USA (Tikr.com)

Literally, in each Letter to investors:

We patiently wait for a better price or a better business to purchase because we are playing a long game, where even three years is just a first step. We want to demonstrate that time in the market means more than timing the market. The Fund mainly invests in solar, wind, and other sustainable products and services. Sometimes those kinds of businesses appear too pricey to risk the Fund’s money. So, we also search for sustainable Tech, IT, and Consumer companies.

Management discussion

Last year granted us the ease to discuss the returns; the Steppe Eagle fund finished 2025 +31.71%. It was quite grim to keep a cautiously optimistic grin in late 2024 – early 2025, after a disappointing 2023-2024. Nevertheless, we stayed true to the long-term prospects of the investment portfolio, despite losing a few valuable Unit holders, so we are sincerely thankful to those who stayed.

The Fund’s recovery stood on two whales: the end of the bear market in the clean energy sector, hopefully, and the strong performance of a few IT bets we had for several years, like Alphabet and Shopify. We can’t see the future, but we see that the success of these stories is far from over, because we try to stick to multi-decade super trends that are shaping our world.

Our principles are:

- No debt or derivatives;

- No shorting;

- No market timing;

- No index hugging;

- No agitation about short-term fluctuations;

- No diversification for the sake of diversification.

Sector rotation in the stock market takes years, if not decades, to turn a full cycle: from Energy to Financials through Basic materials and Consumer Discretionary. Thus, as the solar energy sector takes a bloodbath once every 10-15 years, and we had one in 2023-2024, we should have a rough but mind-blowing road ahead.

A few historically strong companies were taken in 2025, which had traded at sky-high multiples. However, in 2025, their valuation finally matched reality, and that is how good long-term investments are usually made. Sure, time will point out the mistaken purchases, which is okay given that the right choices cover them with excessive profit. Adobe over 4% of portfolio at $336-386 range; Nextpower over 3% in a $37-43 range; Magna International over 3% at $32; Uber and Lyft over 2% of portfolio each, at $70 and $13, respectively. And several less significant: Fluence Energy, Puma SE (PMMAF), Shoals, Thor Industries, Vestas Wind Systems.

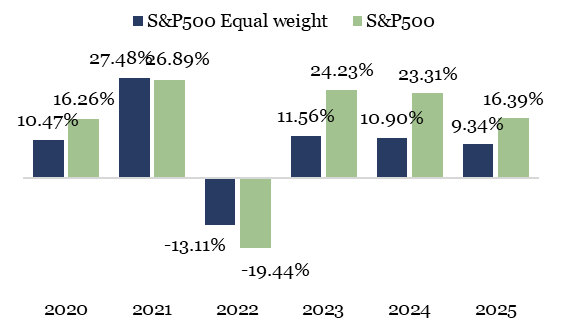

Yet another year of funny market behavior: the growth of just specific sectors and companies, not an economy-wide elevation. It doesn’t look healthy and has more in common with sports betting or casinos than it should. Technology, Communications, and Industrials, all about data centers and electricity. And that feels more like a religion than a reasonable forecast; you can judge it by comparing the results of an equal-weight S&P 500, where all companies have the same weight in the composition, and the usual market cap. weight, S&P 500 (in the chart below). Because these five hundred companies represent around 80% of the United States economy, their juxtaposed performance should be distributed more fairly. The last three years don’t look right.

Market cap vs Equal weight (Yahoo Finance)

The portfolio benefited from the following:

The gross investment income in FY 2025 was $112 000, which resulted in +41.88% return and +31.71% net of fees, including the Success fee. And the heavy hitters were solar energy equipment companies, IT: Data & ecommerce, and industrial companies as a cherry on top. Combined, the Clean energy companies had the strongest impact when all the bits are scrapped together.

Company

Ticker

Return, since purchase

Change

Shopify Inc

SHOP

16,975.05

364.08%

Alphabet Inc

GOOGL

13,924.93

197.63%

SMA Solar

S92, SMTGF

9,261.74

161.21%

Nextpower Inc

NXT

7,438.31

114.45%

CRM

4,363.37

42.75%

Click to enlarge

Most of the clean energy names doubled since Dec31 2024, if not tripled, which either resulted in substantial profit, or recovered a significant part of the previous loss.

The portfolio suffered from such miscalculations:

Unfortunately, our old, unreliable friend, the wind energy blades producer TPI Composites (TPICQ), decided to file for bankruptcy. We were lucky to sell 95% at $1.87 during 1H 2025; the last price for Dec 31, 2025, was $0.0115. As the overall impact since the purchase was large, in 2025 alone, due to a 95% liquidation of the position at a price above the Dec 31, 2024, price ($1.56), it actually turned into a small gain. We didn’t have serious detractors of performance in 2025, only the accumulated loss from previous years.

Company

Ticker

Return, since purchase

Change

TPI Composites

TPICQ

-13,394.15

-99.53%

Solaredge

SEDG

-9,306.02

-75.44%

Enphase Energy

ENPH

-5,613.53

-71.45%

PUMA SE

PUM GR, PMMAF

-3,046.67

-49.23%

Click to enlarge

Our motto: bring returns through intelligent investing into friendly to the environment and shariah-compliant businesses across developed economies.

- The companies that are already mature enough to function with numbers close to or well beyond one billion US dollars;

- Which already faced and coped with crises in the past;

- Can efficiently operate without excessive debt;

- Companies who practice excellent financial health;

- Work in agreeable industries, especially clean energy, recycling, conscious consumer goods and services, IT and software;

- Businesses that Mr. Market is occasionally offering with a significant discount to intrinsic value;

- Totally having in mind Mr. Buffet’s saying: “Our favorite holding period is forever.”

Stocks are not lottery tickets. There is a company behind every stock. When the company does well (grows revenues, profits, and cash flows), the stock usually follows. We often miss the right timing (that is reserved for fortune tellers); however, if figures and facts do not deteriorate, they show up in the price in their due time.

The following data describes the state of the portfolio on December 31, 2025.

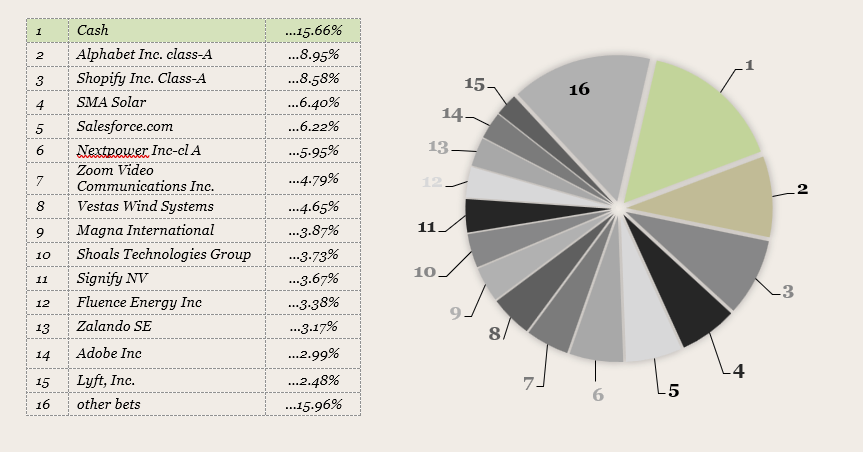

Composition of the portfolio by position:

Composition of the portfolio by position (Harry Qelm Baabsman Ltd.)

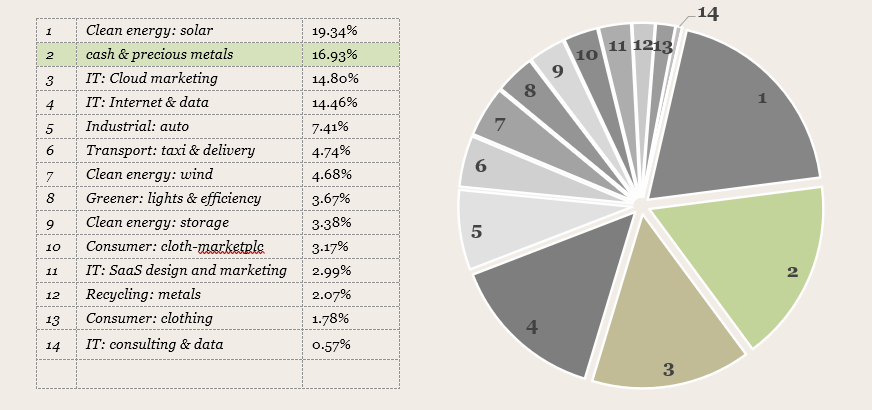

Composition of the portfolio by industry:

Composition of the portfolio by industry (Harry Qelm Baabsman Ltd.)

We should also describe our view on several promising stories:

Salesforce: The company pioneered cloud-based CRM systems (Customer relationship management). Its bright leadership by Marc Benioff and famous corporate culture enabled it to cultivate a team of talented professionals who develop several important platforms that help businesses globally to work with clients, make analytics and decisions, and develop new connections. That is a big company with sales of over $40 billion; Salesforce’s business is growing at a double-digit pace, which has shown a few features of maturing, slowing its fast-growth phase, but with rapidly improving profitability (operating margin jumped from 2% to 20+% in just four years) and a healthy balance sheet. Our average purchase price is $186 in 2023. Everybody seems to like CRM’s visionary role and wide range of integrated and interlinked solutions. The company’s stocks deserve a hefty 6% to 8.5% portion of the investment portfolio and a prolonged holding period, over 7 years or more. Widely discussed the potential demotion of SaaS companies due to LLMs’ progress, but let’s wait and see.

Alphabet Inc: The one from the Tech Titans that the Steppe Eagle has under his wing. This behemoth commands a Sales figure of over $400 billion and a market capitalization of over $3.5 trillion. In recent years, the company has kept its grasp over the Internet Search, YouTube, and AI. It also vigorously grows in the area of Cloud Computing (double-digit growth), and this is the top company for Autonomous Driving, an undisputed leader with the most driven distance. It still doesn’t look expensive and is worth every invested dollar. We entered the position in 2022 and 2023 at an average price of $106.

Zoom Video Communications (ZM): We consider Zoom as a business with a great product and a talented team that learns from mistakes and develops more and better future products. It came from a Zoom call to Zoom workplace; it is so much more now than just a video-conference software company. Today it is a sustainable, profitable business with a bright idea, which was an exceptional pearl even before COVID-19. The debt level is low, the revenue stream continues to come above $4.9 billion a year, the business has a 30+% free cash flow margin and its product canceled millions of unnecessary business travel, which is very green. Zoom has some difficulties growing again at a double-digit pace, but when it fell to below $60, it was an opportunity to step heavily in. Now, the company is trading more reasonably between $75 and 90. It is a nice long-term business to hold.

Zalando SE (ZAL GR), (ZLDSF) : Is a 12+ billion EUR in sales European e-commerce clothing retailer with a stiff grip over the EU market. Financially healthy but with a thin profit margin, this clothing retailer is a leader that could bring stable double-digit growth for the portfolio over the years. The least exciting part about this business – it is less green than we previously thought because Fast-fashion is not green, even with conscious execution. We believe the company is undervalued, and we shall eventually see its recovery. In 2025 its price declined from 35 EUR to just 22 ignoring growing underlying business. Revenue’s compounded annualized growth rate or CAGR for the last 5 years was 9.1%, and earnings per share continued to come out sturdy. In the next 3-5 years we expect further recovery of this business towards more robust numbers and growth.

Nextpower: The business manufactures solar tracking systems primarily in the USA; these systems allow solar panels to follow the sun disk through its daily orbit, which increases the solar energy output by 25-40%. It is a Flex Ltd spin-off, with $3.5+ billion in annual sales, which demonstrated growth when all other solar companies faltered in 2024 year; it expected to grow at a 20-30% pace for the next several years; the profit margin is dancing between 10% and 17%; and the debt is just $45 million at total assets of $3800 million. The shares of this company have been trading just for a few years, which is the only reason we hesitated to have more than 5% of this company in the portfolio. We prefer 10+ years of history. Our average entry point in 2024-2025 is $40.

Signify NV (LIGHT NA) (SFFYF): Previously known as Phillips Lighting, it has declining annual sales of 6.1 billion EUR. Still, it pays a truly handsome >5+% dividend at current prices (20-22.5EUR) because during the phase of slowing sales it amends the business to make it leaner and more effective. The company was offered by Mr. Market between 0.4 and 0.45 levels of the price-to-sales ratio. In contrast, the usual and fair valuation should be between 0.6 and 0.75 price to sales. Everyone knows Phillips’ lighting solutions, and everyone who has bought lamps for their homes or cars. Additionally, the company is constantly fighting for better efficiency of its lighting products, developing greener and futuristic solutions to illuminate our lives. We would like to keep this business as long as possible if it continues to operate with a lower debt level. At some point in time, the decline is expected to be over, and slow recovery must situate this business from 21EUR closer to 30EUR.

Vestas Wind Systems: Vestas is a poster child of wind energy; it is the largest and oldest among currently active companies. All major wind energy markets across the globe, except for China, are served by Vestas. Its revenue and asset base are colossal for the clean energy sector. The company is contracted for 5 years ahead, 27GW of projects in the pipeline, and 37 billion EUR of service contracts. The problem with a thin Profit margin that overshadowed this company previously is gone now. In 2025, the company achieved record sales, kept a healthy balance sheet, and improved adjusted FCF above 1.5 billion (Net Income 778 mln). Our average price is 17EUR. Vestas is a long play, God willing, for several years if they continue keeping the financial health & dominant market position. Our pessimistic model indicated a fair value between 19 and 25 EUR, which was hit in 2025, but we’re not leaving.

Puma SE: The company is a well-known quality brand of specifically footwear and various sports apparel. Its annual sales are at 7+ billion EUR, it has a loyal fan base; however, the business stopped growing in 2024-2025. The same process is happening with Nike. Its fraternal rival, Adidas, is doing considerably better. In 2025, any commercial progress was taken off the table by the economy. Management declared a decline in sales and a “3-year transformation” plan, which honestly can go either way, so we decided to cut the position down to 1% and keep it tiny. German apparel brands are also much more sustainable than others, and Puma is serious about it. We are hopeful that the new CEO (former Adidas executive) will turn the tables. Our average entry point in 2025 was 24.52EUR.

Adobe: The company offers universally renowned graphic design products, such as Adobe Photoshop, as well as digital contract signing tools and marketing products, aiming to leverage them all through LLMs. It has a tight grip on digital content through editing, signing, and marketing applications. This business has long been characterized as a solid, reliable, 10%-growing business with one of the best profit margins in the industry, above 25%. It deserves its place in the portfolio with a decent growth profile and stability. The main concern for the market is that LLMs, Figma (FIG), and Canva will sooner or later rip Adobe from its growth and premium. This is literally the most profitable among big tech companies, with $24 billion in revenue and a stable 36+% operating margin, which Mr. Market is offering at unheard-of since the 2010s multiples of PE and P/FCF. We are holding a 3+% position with an average buying point of 336.

Silver & Gold: These two monetary metals simply serve as a bank account as a hedge and shelf for unused cash. We still keeping a little of both since 2022.

SolarEdge (SEDG): This fast-grower is unfortunately prone to cycles. Producer of power optimizers and string inverters for solar energy generation. We have followed the company since 2017 because it used to manage to increase revenue by 25-35% every year, operating profit too, using a considerably small amount of debt. The company works in both great solar energy markets (the United States and the European Union). SolarEdge and Enphase (ENPH) are leaders in this business. Yet, crisis 2024 made evident issues with the company, such as unnecessary product diversification and weak control over profit margin, so the cycle forced the business to change its CEO and CFO. The business showed signs of recovery, and the stock price changed from $13 to $33-39 in 2025. However, our average position is still $117.5.

SMA Solar: Before SolarEdge and Enphase, the solar inverters market only knew the commendable name of SMA Solar AG, the stable German company. It has been through many cycles; it lost the North American market to the aforementioned companies, but was able to compete in Europe. The company makes EUR 1.5+ billion in revenue, has long-term contracts on its home turf, 11% debt-to-assets ratio, and enough cash to weather a storm. It never dilutes its shareholders. On the downside, the profitability has been lost, so only the ongoing recovery could fix it. We were fortunate to buy at EUR14.21 in late 2024, for less than 2.9% of the portfolio; now it is over 6%. Price has more than doubled.

The pleasure of investing in such companies is all ours. We are sincerely thankful to The Steppe Eagle’s Investors for their patience and courage. It helps us to keep focused on investing in all market weather.

Conclusion

We are perfectly aware that nowadays, investors have tons of fund and fund manager options. These institutions issue all sorts of “Letters to Shareholders,” mimicking the world-renowned Buffet’s letters. Why is our letter different? Well, we are neither the smartest nor the luckiest fund managers, so we can’t preach accounting practices or deep economic theories. Yet, we have something unique we can share because we gathered all the mistakes we made throughout our careers in one text, and we can publish it bit by bit every year. The first hard lesson we published in the 2022FY report was: “The first most frequent and painful mistake is buying too soon. Let stocks fall!”. In practice, that works as such: When you find an asset you are intrigued to invest in, don’t buy it right away. Wait another couple of months and try some. Then, wait another 3-6 months to add some more. Sometimes, you can wait for years.

This time we share the second hard lesson: “If the current management promises keep drifting away from actual financial results – run away because these people don’t know what they are doing: your investment is seriously endangered by the lack of integrity and transparency.” That rule is simple – if the company has problems, the management must be open about it to show a realistic plan to overcome them and give investors enough data to manage expectations. If they don’t, it means they cover up something unpleasant, and you shouldn’t learn this out the hard way. TPI Composites (TPIC) is a vivid example of this rule.

For the FY2024 we feel obliged to talk about the third hard lesson: “Selling whenever it gets back to breakeven”. It is opposite to the first lesson. We, investors, do not know when a stock stops going down – purchasing falling knives involves the pain of waiting for the stock to finish its decline. More often than not, it crumbles much further than you initially anticipated. Naturally, when it returns to the previous price levels, an investor feels compelled to sell the “bad choice” at the first most minor profit or break even. Most times, the story only starts there. If your reasoning for the purchase remains the same, you should keep this investment and see what happens in a year or two. Miracles are not so rare.

Another year – another lesson, the fourth hard lesson: “Must always have 25% in cash/gold, except for brief moments after big drop spending (for instance, April 2025, 4q 2024, 3q 2022). When -50-70% declines happen, and they certainly will, the best thing is to have more cash at hand. That was a blessing to have expandable cash when Nextpower was offered at $37 ($110-120 now), or Uber and Lyft at $69 and $13, respectively ($90 and $22 in late 2025). And that felt so bad, without much cash when Corona-crash happened in March 2020.

Thank you for reading!

This article was written by

Analyst’s Disclosure: I/we have a beneficial long position in the shares of GOOGL, CRM, ADBE, SHOP, ZM, MGA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

All rights reserved. The Steppe Eagle OEIC is purposed for long-term Professional investors who possess no less than $150 000 in Net Assets and can invest $50 000, according to a set of definitions provided by AIFC laws. Distribution, copying, and modification of materials without the written consent of Harry Qelm Baabsman ltd are prohibited. This Investment Report contains general information about The Steppe Eagle OEIC ltd, managed by Harry Qelm Baabsman ltd as Fund Manager, and is intended for informational purposes only. This report was prepared by Harry Qelm Baabsman ltd. Harry Qelm Baabsman ltd shall not be responsible for any liability arising from using the information in a twisted corrupted, or misleading manner. The value of Units/Preferred shares of the Fund, as a result of a change of asset prices in its Net Assets Value (NAV), can both increase and decrease. Investment performance in the past does not determine future returns. Neither the Fund manager nor any of its directors, officers, or employees guarantee the return on investment in the Fund's (The Steppe Eagle) units.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Source: Harry Qelm Baabsman's 2025 FY Letter To Investors – Read full article at Seeking Alpha